I had the unfortunate experience this week of watching my coworkers (and friends) get called to the "new" bosses office one by one to receive there walking papers. As each person did (to quote one of them) "the walk of shame", the rest mingled about wondering who was going to be summoned next. It soon became apparent as we mingled that this layoff would be far more reaching and "transformitive" than we had expected. In the end 6 out of 9, including the "old" boss where relieved of their jobs.

In nearly 15 years of work i have never been this close to a major layoff. Often in the past you would have an idea who was going to get whacked because they often where slackers or had some issue working with people. This time seemed different.

The callousness of management to the whole matter was just shocking. Especially since many months of time and effort before this event were spent telling us how it was important to have integrity and that they were managing the company with integrity. Several weeks of consistent lying have shattered any illusions about managements intentions. In the end we are all pawns to be used up and spit out when we are no longer useful.

What is odd about the whole situation is that in my 15 years of work i have been through as many layoffs, but have never been affected until the last year. I was laid off from my previous employer not even a year ago and then nearly laid off from this one. I do not know if it is a sign of the times in general or something specific to engineering, but either way I do not want to be caught in this situation again.

I finally realize that in spite of all the education and experience i have, that i am just a factory worker. I have a job not a career. It is this realization that inspires me to find a solution to the problem of having to work for people like this, but for now I have a job and it's a job I'm lucky to have.

--Staff

Friday, February 13, 2009

Tuesday, February 10, 2009

What an awesome plan!

Well the latest plan from Treasury Secretary Timothy Geithner did not impress the markets today. I think the plan put forth was in fact not a plan at all. The primary reason for the sell off (beyond the resistance at the 50 day moving average) was that the market could see that they have no plan to "fix" things. It actually seems odd that they bothered having a news conference at all, given the lack of details. Maybe they figured they better just say something since they have been alluding to a new plan for sometime. Just as Obama is pushing for the stimulus with the argument "we need to do something?" , he must have forced the treasury to just do something as well.

Unfortunately the problem of bad assets is not easily solved. The ideas put forth look very similar to the original TARP plan which was abandoned. The problem is simple. If you buy the banks bad assets what do you pay? If you pay too much you have little effect as you cannot buy very much bad paper and you are sure to incur large losses for taxpayers. If you pay too little the banks need to write down the assets to the price paid which could deplete their capital more and maybe reveal they are insolvent. This is why the "bad bank" ideas will not work as envisioned.

I suppose looking back at the Resolution Trust Corporation method you should be able to help the situation. But the thing is those assets came from banks that were closed, hence the government accepted they were insolvent. The real issue now is that no one wants to admit the banks are insolvent. The reason I'm guessing is because of all the derivatives.

The derivatives essentially link all the banks together so tightly that if one fails, they all fail. These derivatives are very diverse and are not limited to housing. This is one of the fallacies of the view that "if we fix housing everything will be okay." My guess is that many of these derivatives are nothing more than side bets. Think of the movie Caddy Shack where the guys are behind the bushes and betting on if the kid will pick his nose, then eat it.

Now side bets are fine if you have the money to lose, but it is becoming apparent they bet with borrowed money. Even if you win the bet, if the person you bet against can't pay, you lose. So the issue is all these banks made extremely large bets with each other. If anyone of them goes down they take out the others because the losers can't pay. Also it highlights that the banks may not have diversified their bets very well either. If a bank tried to be a little conservative and hedge some big bets, but the guy that took the hedge went out of business, you have no hedge at all. Or if they were arbitraging in some way by betting both sides but getting (in betting parlance) some "juice", if one or both sides can't pay, the surefire can't lose bet is a bust.

The crux is that this is bigger than housing. This is part of a larger speculative debt bubble and it will take more than a few talking heads talking in vague terms to get through this.

--Staff

Unfortunately the problem of bad assets is not easily solved. The ideas put forth look very similar to the original TARP plan which was abandoned. The problem is simple. If you buy the banks bad assets what do you pay? If you pay too much you have little effect as you cannot buy very much bad paper and you are sure to incur large losses for taxpayers. If you pay too little the banks need to write down the assets to the price paid which could deplete their capital more and maybe reveal they are insolvent. This is why the "bad bank" ideas will not work as envisioned.

I suppose looking back at the Resolution Trust Corporation method you should be able to help the situation. But the thing is those assets came from banks that were closed, hence the government accepted they were insolvent. The real issue now is that no one wants to admit the banks are insolvent. The reason I'm guessing is because of all the derivatives.

The derivatives essentially link all the banks together so tightly that if one fails, they all fail. These derivatives are very diverse and are not limited to housing. This is one of the fallacies of the view that "if we fix housing everything will be okay." My guess is that many of these derivatives are nothing more than side bets. Think of the movie Caddy Shack where the guys are behind the bushes and betting on if the kid will pick his nose, then eat it.

Now side bets are fine if you have the money to lose, but it is becoming apparent they bet with borrowed money. Even if you win the bet, if the person you bet against can't pay, you lose. So the issue is all these banks made extremely large bets with each other. If anyone of them goes down they take out the others because the losers can't pay. Also it highlights that the banks may not have diversified their bets very well either. If a bank tried to be a little conservative and hedge some big bets, but the guy that took the hedge went out of business, you have no hedge at all. Or if they were arbitraging in some way by betting both sides but getting (in betting parlance) some "juice", if one or both sides can't pay, the surefire can't lose bet is a bust.

The crux is that this is bigger than housing. This is part of a larger speculative debt bubble and it will take more than a few talking heads talking in vague terms to get through this.

--Staff

Friday, February 15, 2008

the current market condition

I talked earlier about the qqqq's (nasdaq100) putting in a potential double bottom, while the other major indices, the spy(s&p500) and the dia(dow30) had not. This divergence creates a dilemma. In the past my experience shows that divergence in the major indices often does not last long. So will the qqqq's break below the support and the spy/dia come down to support and create a double bottom, or will the qqqq's tread water until the spy/dia come down to support, or will the spy/dia rally created a racing double bottom (a double bottom with the right leg down not going all the way down to the support level)?

Now it is becoming a little more clear. The qqqq's have not created a double bottom. The spy and dia are starting to form a symmetrical triangle (see here for a definition http://stockcharts.com/school/doku.php?id=chart_school:chart_analysis:chart_patterns:symmetrical_triangle )

Now the symmetrical pattern often is a continuation pattern, which means once completed the stock continues it's move up if in an uptrend or down if in a downtrend. But often it is a reversal pattern, which means the stock changes direction from up to down or vice versa. Generally if the trend is not well established, meaning the trend has not been in place for a long time and is not well defined, then the possibility is that the pattern will be a reversal. Here is a chart of GS that shows this symmetrical triangle as a reversal pattern. Note that in this case there was not a real uptrend just a channeling between 230 and 170 or so. Note that the break out of the triangle's lower trend line was tested when the stock rallied back up into the lower trend line. At the point it failed to break the lower trend line to the upside confirmed the break to the downside.

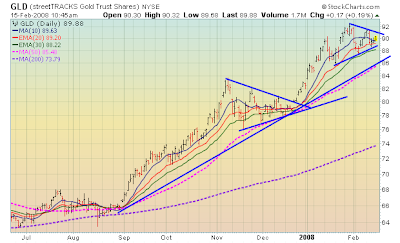

Below is an example of a symmetrical triangle in gld that is a continuation pattern. Notice the triangle that formed in Nov-Dec last year. In this case it broke out of the upper trend line and never tested the trend line. Note in this case that there was a much more well defined trend in place when the triangle formed. Also notice that another triangle is forming as we speak.

The crux of the matter is that it may be difficult to predict the direction the stock or market will move after a symmetrical triangle forms. The most important thing is which way it breaks. It is also nice if it tests (and passes) the broken trend line but as with gld this does not always happen.

Back to the major indices or their tradable cousins their tracking etfs. Looking at the qqqq's we see a potential symmetrical triangle forming. The double bottom never formed. Also there is not a good place to draw a trend line and if you did it would be very steeply down, almost unsustainable down. So now I believe the potential is for the symmetrical triangle reversal pattern to form. Note this pattern is also forming in the dia.

Looking at the dia below we see a similar pattern forming. Although in this case there is a little more definable downtrend line that can be drawn.

The conclusion is that we are now seeing the major indices correlate in that they are all consolidating. They are all making a similar symmetrical triangle pattern. While we cannot know which way we will break from this consolidation, we do know what to look for. We look for a breakout and based on the direction we can get a sense of the direction of the next move. Since these are major indices I would expect a break and then test. If the test confirms the breakout then another significant move up of down can be expected.

On another note. When you look at the gld chart above we see another triangle forming currently. It looks as if it will break to the upside again. But I do have to wonder how much further gld can go without a major correction. It has had a very big run.

--

Now it is becoming a little more clear. The qqqq's have not created a double bottom. The spy and dia are starting to form a symmetrical triangle (see here for a definition http://stockcharts.com/school/doku.php?id=chart_school:chart_analysis:chart_patterns:symmetrical_triangle )

Below is an example of a symmetrical triangle in gld that is a continuation pattern. Notice the triangle that formed in Nov-Dec last year. In this case it broke out of the upper trend line and never tested the trend line. Note in this case that there was a much more well defined trend in place when the triangle formed. Also notice that another triangle is forming as we speak.

The crux of the matter is that it may be difficult to predict the direction the stock or market will move after a symmetrical triangle forms. The most important thing is which way it breaks. It is also nice if it tests (and passes) the broken trend line but as with gld this does not always happen.

Back to the major indices or their tradable cousins their tracking etfs. Looking at the qqqq's we see a potential symmetrical triangle forming. The double bottom never formed. Also there is not a good place to draw a trend line and if you did it would be very steeply down, almost unsustainable down. So now I believe the potential is for the symmetrical triangle reversal pattern to form. Note this pattern is also forming in the dia.

Looking at the dia below we see a similar pattern forming. Although in this case there is a little more definable downtrend line that can be drawn.

The conclusion is that we are now seeing the major indices correlate in that they are all consolidating. They are all making a similar symmetrical triangle pattern. While we cannot know which way we will break from this consolidation, we do know what to look for. We look for a breakout and based on the direction we can get a sense of the direction of the next move. Since these are major indices I would expect a break and then test. If the test confirms the breakout then another significant move up of down can be expected.

On another note. When you look at the gld chart above we see another triangle forming currently. It looks as if it will break to the upside again. But I do have to wonder how much further gld can go without a major correction. It has had a very big run.

--

Wednesday, February 13, 2008

Where i am at.

Over the last several years I have tried to get educated about basically how money works. The more I read the more I realized that I needed to start doing something to try to achieve financial independence. Having read Rich Dad Poor Dad by Kiyosaki and many other books I have started to look at money in a whole new light. While RDPD does not provide any concrete advice on how to get rich or reach financial independence it does provide a framework for understanding how money works. And I believe without that framework it is a losing battle to attempt to secure your retirement or reach financial independence. The reason is that many of the myths bandied around as fact are detrimental to your financial future. But that is a discussion for another day.

As a result of my education one goal of my life is to become financially independent. First what do I mean by financially independent. Well in my case I mean that I have enough passive income coming in every month to cover all my expenses and to provide me a comfortable life (basically the lifestyle I have now + a little bit more free cash). What do I mean by passive income? Well I mean income that I do not have to work for. As a simple example a stock dividend or rent on a building you have professionally managed are examples of passive income. It is income you did not work for. It is income that comes from your money working for you. One thing to note that in some ways a beggar that get's enough to live on is independent, but his income is not passive. If he does not go to work (begging) he makes no money.

If you think about it we all are trying to be somewhat financially independent by retirement. We try to have enough saved so that we no longer work, but have enough income coming from stocks, bonds, and investments to live on. The one catch is that we also hope for social security which makes us very unindependent.

So back to my goal of being financially independent. This is a great goal, but the question is how to do it? Well one thing I have learned the hard way is that this is going to take some time and it is not going to be easy.

One of my first attempts at this was to invest in Oil and Gas Joint Partnerships. Basically companies put together a group of investors to fund the drilling, completion, and production of an oil or gas well. In this case I have had some success and some failures. One interesting note is that I have been left with some concrete assets in the process. I still have two ventures that I do absolutely no work with, but which I get a check every month. This is the definition of passive.

The problem with O&G Partnerships is that they are very hit and miss. You really need to invest large amounts of money spread over many projects to reduce risk. I do not have enough money to do this right. It also will not make you rich. This is my key discovery. The returns of some projects can be huge, but because you need to spread out the money the net returns of your overall investment is much less.

If I had a lot of money sitting in a pile I would invest 20% of it in these projects as net overall I would make a decent return on my money. But earning 20% does not get you financial independence. Also to do it right you either need to hire someone to find and invest or you need to do it yourself which then is a job.

What I have learned is that I need more control over my money. I cannot just hand it to someone and expect them to make me money. There just is no incentive for them to do well with my money.

As a result of this experience my conclusion is that to achieve financial independence I need to start my own business. But what business and how do I do it? Well more to come in my next post.

--

As a result of my education one goal of my life is to become financially independent. First what do I mean by financially independent. Well in my case I mean that I have enough passive income coming in every month to cover all my expenses and to provide me a comfortable life (basically the lifestyle I have now + a little bit more free cash). What do I mean by passive income? Well I mean income that I do not have to work for. As a simple example a stock dividend or rent on a building you have professionally managed are examples of passive income. It is income you did not work for. It is income that comes from your money working for you. One thing to note that in some ways a beggar that get's enough to live on is independent, but his income is not passive. If he does not go to work (begging) he makes no money.

If you think about it we all are trying to be somewhat financially independent by retirement. We try to have enough saved so that we no longer work, but have enough income coming from stocks, bonds, and investments to live on. The one catch is that we also hope for social security which makes us very unindependent.

So back to my goal of being financially independent. This is a great goal, but the question is how to do it? Well one thing I have learned the hard way is that this is going to take some time and it is not going to be easy.

One of my first attempts at this was to invest in Oil and Gas Joint Partnerships. Basically companies put together a group of investors to fund the drilling, completion, and production of an oil or gas well. In this case I have had some success and some failures. One interesting note is that I have been left with some concrete assets in the process. I still have two ventures that I do absolutely no work with, but which I get a check every month. This is the definition of passive.

The problem with O&G Partnerships is that they are very hit and miss. You really need to invest large amounts of money spread over many projects to reduce risk. I do not have enough money to do this right. It also will not make you rich. This is my key discovery. The returns of some projects can be huge, but because you need to spread out the money the net returns of your overall investment is much less.

If I had a lot of money sitting in a pile I would invest 20% of it in these projects as net overall I would make a decent return on my money. But earning 20% does not get you financial independence. Also to do it right you either need to hire someone to find and invest or you need to do it yourself which then is a job.

What I have learned is that I need more control over my money. I cannot just hand it to someone and expect them to make me money. There just is no incentive for them to do well with my money.

As a result of this experience my conclusion is that to achieve financial independence I need to start my own business. But what business and how do I do it? Well more to come in my next post.

--

Exited the qqqq's

While i needed to go out of town and did not feel comfortable leaving my long qqqq positions on so i exited Friday of last week. We still appear to be in the same position as last week. We may be forming a double bottom on the nasdaq 100. We also may be forming a double bottom on the S & P 500 as well. In this case the double bottom would be distorted in that the second low did not make it all the way down to the first low. This is actually a position sign.

Before i rush out and buy a bunch of stuff i need to understand if this potential double bottom is different from the one put in on March of last year. One difference is that at that time the 50 day moving average was above the 200 day average. This is a more general bullish indicator for longer term institutional investors. Right now things are different in that the 50 is below the 200 and both a pointing down. Another differnce is that in March the market was in a consolidation period for 3 months before the double bottom formed. Right now we are clearly in a decline not a consolidation period.

My guess is that if the bottom forms we have limited upside potential. I keep trying to figure out what is the near term target we could expect. Getting to 13000 on the dow seems the furthest we could go at this time. What is the impetous to get to 14000 again? So for now i will sit out and watch. I do have a small gold position i am sitting on. It is starting to look like a symetrical triangle is forming. Although this will be smaller than the one that formed in Nov-Dec of last year, this sets up for a possible further rise. As always we don't know until the pattern completely forms and then breaks out. If it breaks lower then i'm out.

--

Before i rush out and buy a bunch of stuff i need to understand if this potential double bottom is different from the one put in on March of last year. One difference is that at that time the 50 day moving average was above the 200 day average. This is a more general bullish indicator for longer term institutional investors. Right now things are different in that the 50 is below the 200 and both a pointing down. Another differnce is that in March the market was in a consolidation period for 3 months before the double bottom formed. Right now we are clearly in a decline not a consolidation period.

My guess is that if the bottom forms we have limited upside potential. I keep trying to figure out what is the near term target we could expect. Getting to 13000 on the dow seems the furthest we could go at this time. What is the impetous to get to 14000 again? So for now i will sit out and watch. I do have a small gold position i am sitting on. It is starting to look like a symetrical triangle is forming. Although this will be smaller than the one that formed in Nov-Dec of last year, this sets up for a possible further rise. As always we don't know until the pattern completely forms and then breaks out. If it breaks lower then i'm out.

--

Thursday, February 7, 2008

long and strong? Not really.

Well i started taking some light long positions in the qqqq's today. I am doing this because we are in the process of testing the January lows in this ETF and i believe it is likely we will see a bounce here. I am not very confident as this market is brutal, but I'm stuck dipping my feat in somewhere.

I think the biggest concern I have is that the nasdaq 100 (qqqq etf) is the only major average that is at the January low. The S&P 500 and dow jones industrials still have some ways to go before hitting the lows in January. So we have a divergence here. The fact is the tech stocks as represented by the qqqq's have been beat up a little bit more than the rest of the market. That is why they are already back to test the January low. So will the tech stocks lead a bounce here or will they mark time while the other averages decline further to catch up? This is impossible to say, but i do know we are at some significant support on the qqqq's.

If you look at the January low it was a little below 42, but this is also the low put in on March of last year. In March a strong double bottom formed and the ensuring rally raged all the way to 55. Given the level of support going all the way back to March of last year and the action today which saw a significant rally before the bears took some shots, I think that this level is not going to just be sliced through without a fight.

I'm not calling for any long term rise in stocks from here, even though you can see if this level holds you could form a double bottom, I'm just looking for a rapid short cover rally which should last no longer than the last one. If we break 42 we have to bail.

The other concern is the bond insurance companies. If more finally get downgraded or someother really bad news comes out this could trip things up pretty good. But i have to think that some of this is starting to get priced in.

--

I think the biggest concern I have is that the nasdaq 100 (qqqq etf) is the only major average that is at the January low. The S&P 500 and dow jones industrials still have some ways to go before hitting the lows in January. So we have a divergence here. The fact is the tech stocks as represented by the qqqq's have been beat up a little bit more than the rest of the market. That is why they are already back to test the January low. So will the tech stocks lead a bounce here or will they mark time while the other averages decline further to catch up? This is impossible to say, but i do know we are at some significant support on the qqqq's.

If you look at the January low it was a little below 42, but this is also the low put in on March of last year. In March a strong double bottom formed and the ensuring rally raged all the way to 55. Given the level of support going all the way back to March of last year and the action today which saw a significant rally before the bears took some shots, I think that this level is not going to just be sliced through without a fight.

I'm not calling for any long term rise in stocks from here, even though you can see if this level holds you could form a double bottom, I'm just looking for a rapid short cover rally which should last no longer than the last one. If we break 42 we have to bail.

The other concern is the bond insurance companies. If more finally get downgraded or someother really bad news comes out this could trip things up pretty good. But i have to think that some of this is starting to get priced in.

--

walking away and the quitclaim deed

I am reading over and over again the efforts of some counties to force banks or homeowners of homes that have been abandoned to pay to clean or keep up the place. In the case of a homeowner who has stopped paying a mortgage and moves it is not always the case that the bank takes the home back.

You as the homeowner own the home. It is titled in your name. The urban myth that the "bank" owns the home is not true. They have a security interest in it, the mortgage, but do not own it. Just look at the county title records for proof of this. The result of this is that if you abandon the home you are still responsible for it until the bank formally takes it back. But what if they don't?

There are more reported cases of banks not taking the homes back because they "lost" them or just don't want to pay for the process of getting them back. So who owns it? Well the original homeowner still owns it. As such you are still responsible for taxes and upkeep. In these cases homeowners are being dragged into court to pay maintenance costs the city incurs to keep the home from becoming dilapidated.

So if you are considering walking away what can or should you do? Well first you need to consult a lawyer and a CPA. You need help on the legal and tax consequences of the decision. In addition one small thing to consider if you live in a state that has this type of deed is the quitclaim deed. In California the quitclaim deed simply states that the grantor (the homeowner filing the claim) gives up any interest in the property. Now I am not a lawyer and am not giving legal advice, but the point is this may help assure you have at least a record that you gave up all claims to the property.

In this case it may create many weird issues because this deed just releases claim to the property, it does not really transfer interest such as with a grant deed. So when you bought the place you got title via a grant deed, you relinquish title, and then who has title? I'm sure the lawyers would have a field day with it.

--

ps - see a lawyer if you are considering walking away. if you do this you cannot undo it. So if things should turn around you won't be able to claim ownership or sell it or anything else.

Subscribe to:

Comments (Atom)